從蒸汽機的轟鳴到網際網路的無聲革命,科技浪潮總是在不知不覺間重塑世界的樣貌。

如今,我們正站在一場更為澎湃的科技變革前夜——人工智慧開始「思考」,機器人走出工廠圍牆,半導體逐漸成為智慧時代的「新石油」,而太空則從遙不可及的夢想變成嶄新的商業疆域。

以現在的角度來看,哪些技術將定義未來五年甚至十年?

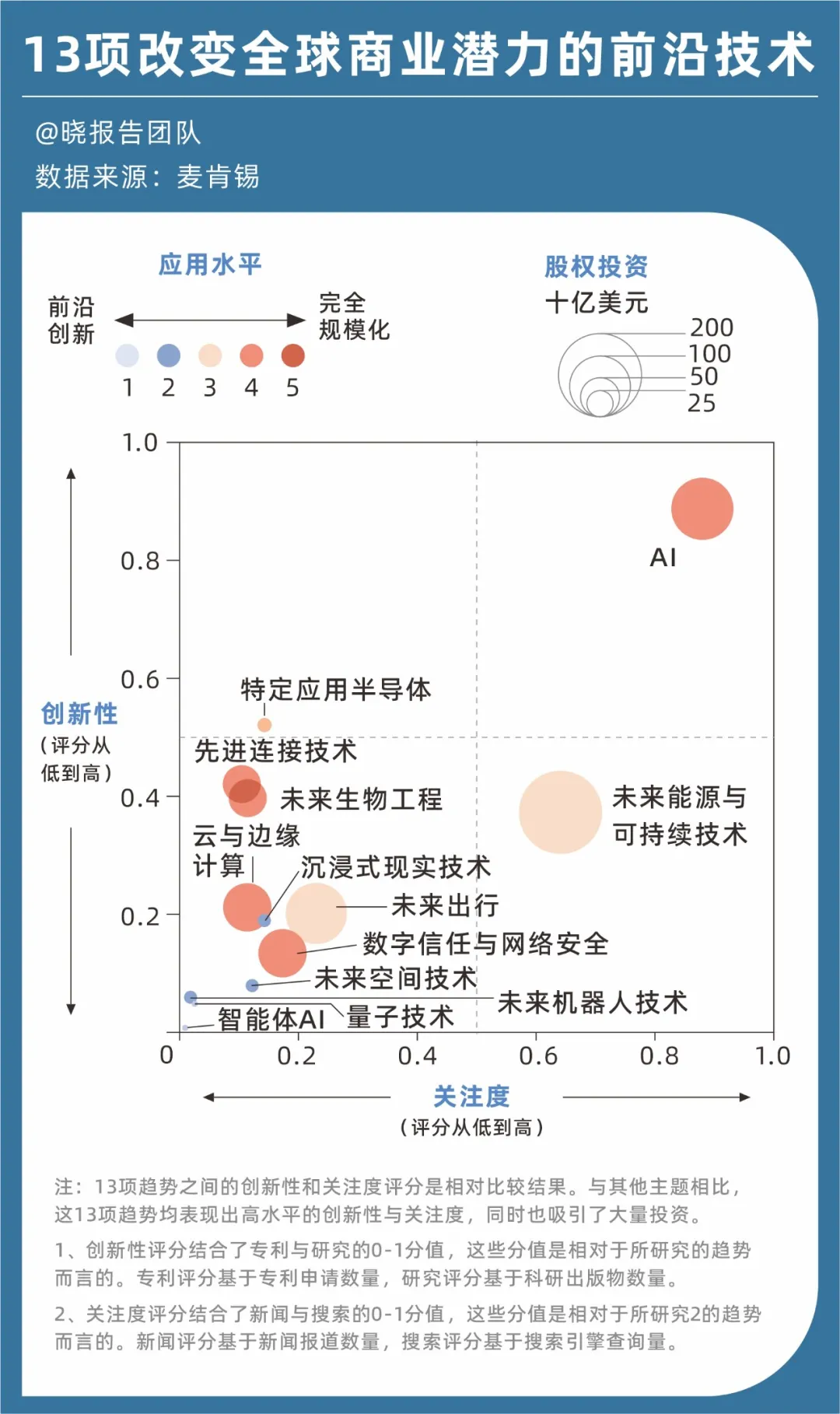

麥肯錫最新發布的《2025 年技術趨勢展望》報告,試圖回答這個問題,提出 13 項具備改變全球商業潛力的前沿技術趨勢,並從創新性、關注度、資本投入及應用水平四大面向,勾勒出這些技術的發展藍圖。

放眼望去,資本高度集中於 AI、未來能源與永續技術、未來出行等正從技術突破邁向深度應用的領域,其中 AI 無論在關注度或創新力上皆遙遙領先。

相較之下,特定應用半導體、先進連接技術、未來生物工程、雲端與邊緣運算、數位信任與網路安全等技術雖然熱度不及 AI,但已悄然成為數位社會運作的「基礎設施」,應用規模逐漸擴大。

至於沉浸式實境技術、未來空間技術、未來機器人技術、量子技術、AI 智能體等,則仍處於孵化階段,但革命性潛力已逐漸顯現。例如 AI 智能體成為今年成長最快的熱門趨勢之一,2024 年股權投資達 11 億美元,年增幅高達 1562%。

參觀者透過 AR 眼鏡體驗雲岡石窟

事實上,無論是哪項技術趨勢,都將重塑產業格局,更已成為國家與企業不可或缺的競爭籌碼。

在中國,這些技術已納入面向 2035 年的未來產業重點賽道目錄,並訂定明確的發展目標。以未來空間技術為例,2030 年中國市場規模有望突破 8000 億元,重點發展方向涵蓋載人低空飛行、深空深地深海探索、極地開發等。

在此,我們整理麥肯錫報告的關鍵資訊與數據,與大家分享這些技術的前沿動態、發展趨勢及人才需求。

13 個賽道與兆元商機

針對這 13 項前沿技術,麥肯錫依其內在「性格」將其分為三大類:AI 革命、運算與連接前沿,以及尖端工程。

這三大技術類別,一個負責「思考」,一個負責「連接」,一個負責「動手」,彼此交融、互相激發,不斷描繪出未來十年科技浪潮的全貌。

◎ 第一類,AI 革命,包括 AI 與 AI 智能體。隨著 AI 影響力持續擴大,值得注意的是,目前 AI 的成本正急劇下降,例如某些推理任務的價格一年內降幅達 900 倍。

針對這兩項細分技術,麥肯錫認為,AI 不僅本身是革命性且具戰略性的技術創新,更能加速其他技術領域的發展,或在跨界領域創造新「商機」,例如 AI 是特定應用半導體的重要催化劑。

而 AI 智能體技術則是今年的熱門趨勢,已迅速成為企業及消費性技術領域的重要發展方向。所謂 AI 智能體,如同一位「虛擬同事」,能自動規劃與執行多步驟任務。

目前,各大公司正於現有 AI 產品中加入智能體功能,或開發全新、專為特定任務設計的應用,尤其在軟體編碼與數學等擁有龐大訓練資料集的領域快速進展。

市場也嗅到商機。MarketsandMarkets 預測,AI 智能體市場規模將從 2024 年的 51 億美元成長至 2030 年的 471 億美元,複合年增率高達 44.8%。

◎ 第二類,運算與連接前沿,這些技術可視為 AI 與數位世界的「骨架」,包括特定應用半導體、先進連接技術、雲端與邊緣運算、沉浸式實境技術、數位信任與網路安全、量子技術。

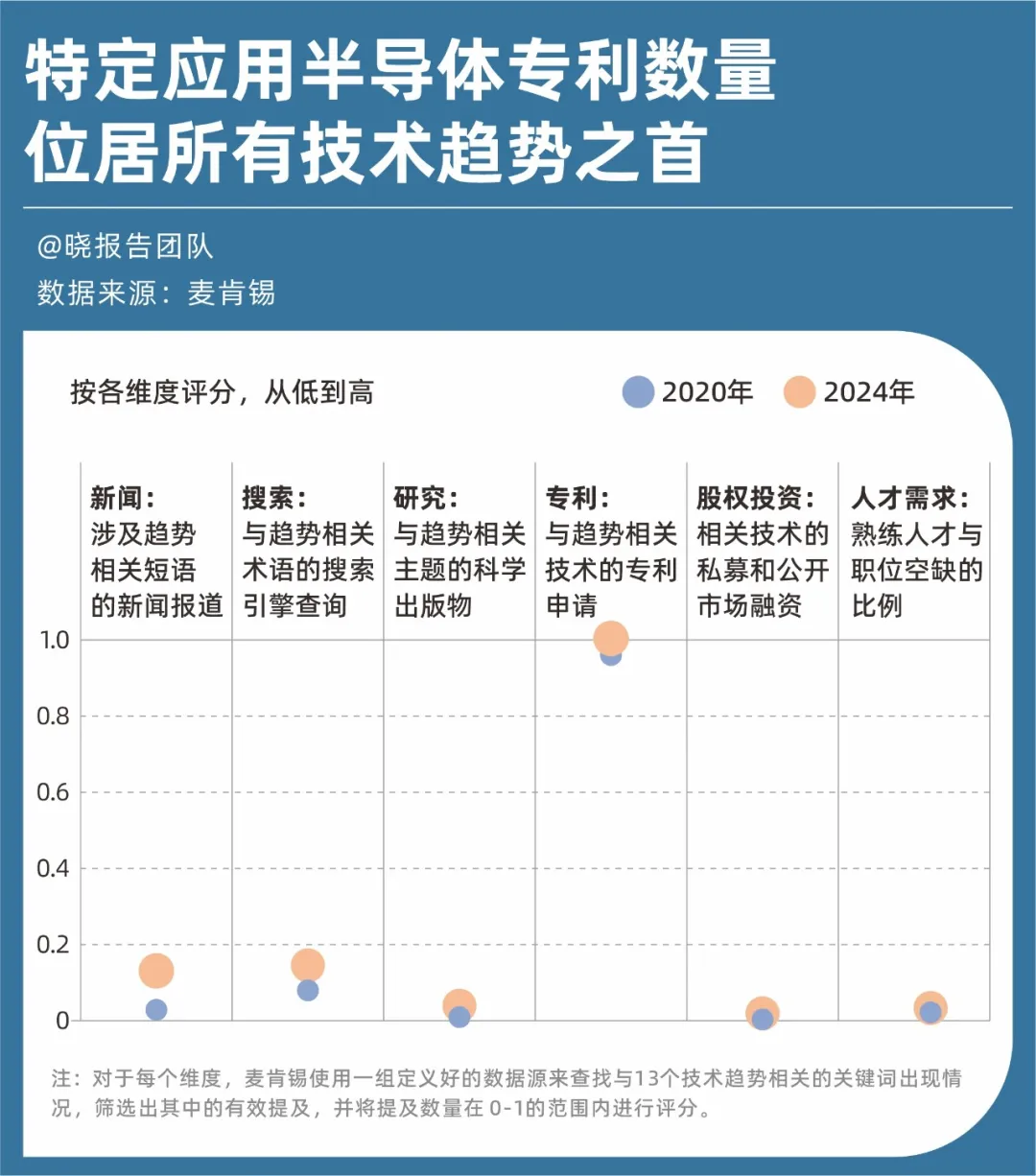

其中,特定應用半導體是報告特別點出的重要趨勢。這些專為 AI 任務量身打造的晶片,正成為科技界的「新石油」——專利數量居所有技術趨勢之冠,去年吸引 75 億美元投資。

同時,AI 的發展對運算能力有著無止盡的需求,仰賴雲端與邊緣運算技術趨勢。麥肯錫研究顯示,到 2030 年,全球資料中心容量需求可能達目前的 3 倍,其中約 70% 來自 AI 工作負載。

此外,在先進連接技術方面,5G 已覆蓋全球 22.5 億用戶,中國在 5G 獨立組網部署居全球之首,而 6G 已在研發中,並將加入「感測」等新功能。沉浸式實境技術領域,AR/VR 應用已從遊戲擴展至醫療、工業設計,Apple Vision Pro、Meta Quest 等裝置亦重新定義人機互動;量子技術雖仍屬前沿,但 Google、IBM、Microsoft 等巨頭已在誤差校正與穩定性取得關鍵突破。

這些技術如同古代絲綢之路上的驛站和道路,雖不直接產生貨物,卻決定商業的規模與邊界。

◎ 第三類,尖端工程,包括未來機器人技術、未來出行、未來生物工程、未來空間技術、未來能源與永續技術。這些技術負責將數位能力「實體化」,讓科技走出螢幕。

過去六十年來,機器人逐漸成為先進製造業的主力,如今逾四百萬台工業機器人在汽車工廠等環境運作。隨著 AI 加速推動,物理機器人技術近年來進入機場、大型商店及餐廳等更廣泛領域。麥肯錫合夥人 Ani Kelkar 預估,到 2040 年市場規模將達約 9000 億美元。

在未來出行領域,中國電動車市場持續成長 36%,自動駕駛、無人機配送與空中計程車也正從概念走向試點,甚至商用落地。預計到 2034 年,商業無人機送貨市場規模將達 290 億美元,年複合成長率高達 40%。

未來生物工程技術則運用基因編輯、合成生物學等技術,改善健康及人體機能、重塑食品價值鏈並創造創新產品。例如基因編輯技術 CRISPR 首度獲得 FDA 核准,AI 也大幅縮短新藥研發成本與時間。2024 年諾貝爾化學獎更頒予三位利用 AI 預測現有蛋白質結構及設計新蛋白質的科學家。

未來能源與永續技術方面,中國不僅在光伏製造居全球主導地位,氫能電解槽產能亦占全球 60%。此外,核能因能提供穩定基載電力而備受關注,31 國承諾至 2050 年全球核能容量增至三倍。

智慧機械手臂協助光伏面板加工

關於這些技術的六大趨勢

透過這 13 項前沿技術的趨勢前瞻,麥肯錫在報告中歸納出六大趨勢,作為技術發展方向之參考。

①自主系統崛起

系統不再只是執行命令,而是能學習、適應、協作。

當 AI 智能體能夠自主規劃工作流程,機器人能適應陌生環境,自動駕駛汽車能於複雜城市路況導航,人類獨特價值主要體現在創造力、倫理判斷、戰略眼光等方面。

無人駕駛汽車已開始商業營運

②新的人機協作模式

人機互動正邁入新階段,特色是更自然的介面、多模態輸入及自適應智慧,讓「操作者」與「共同創造者」的界線逐漸消失。

從沉浸式訓練環境、觸覺機器人技術,到語音助手及感測器穿戴裝置,科技正更精準回應人類意圖與行為。這種演變讓人機關係定位從「機器取代人類」轉為「機器增強人類」能力。

③規模化應用的挑戰

運算密集型工作負載(尤其來自 AI 智能體、未來機器人及沉浸式實境技術)的激增需求,正給全球基礎設施帶來新壓力。然而現實是:電力供應吃緊、晶片供應鏈脆弱、資料中心建設週期長……

這意味前沿技術的規模化應用不僅需解決技術架構與高效設計問題,還要面對人才、政策及執行層面的複雜現實挑戰。這顯示,數位世界的繁榮離不開物理世界的支撐。

技術人員監控半導體生產設備運作狀態

④區域與國家競爭

不可否認,對關鍵技術的掌控已成為全球競爭焦點。中美在晶片、AI、量子技術等領域競爭日益激烈,歐洲則以《人工智慧法案》等規範試圖建立自身數位主權。

技術不再是無國界的公共財,而是國家安全基石、經濟主權象徵。在此態勢下,全球科技合作面臨挑戰,也促使各地區發展自身特色優勢。

⑤規模化與專業化並進

雲端服務與先進連接技術的創新,推動規模化與專業化並行。一方面,龐大且高耗能的資料中心中,通用模型訓練基礎設施快速擴展;另一方面,「邊緣側」創新加速,低功耗技術嵌入手機、汽車、家庭控制系統及工業設備。

這種雙軌發展帶來參數數量驚人的大型語言模型,也推升可於各種場景運作的特定領域 AI 工具日益豐富。

⑥負責任創新的必要性

隨著技術日益強大且更具個性化,信任成為技術採用的關鍵門檻。企業面臨更大壓力——必須證明其 AI 模型、基因編輯技術或沉浸式平台具備透明、公平且可問責性。

道德倫理不再只是正確選擇,更是部署過程中的戰略槓桿。它能加速或阻礙規模擴張、投資決策及長期影響。

資金前景與人才前景流向何方?

以下分析這些前沿技術的資金前景與人才前景,觀察資本與人才正匯聚於哪些領域。

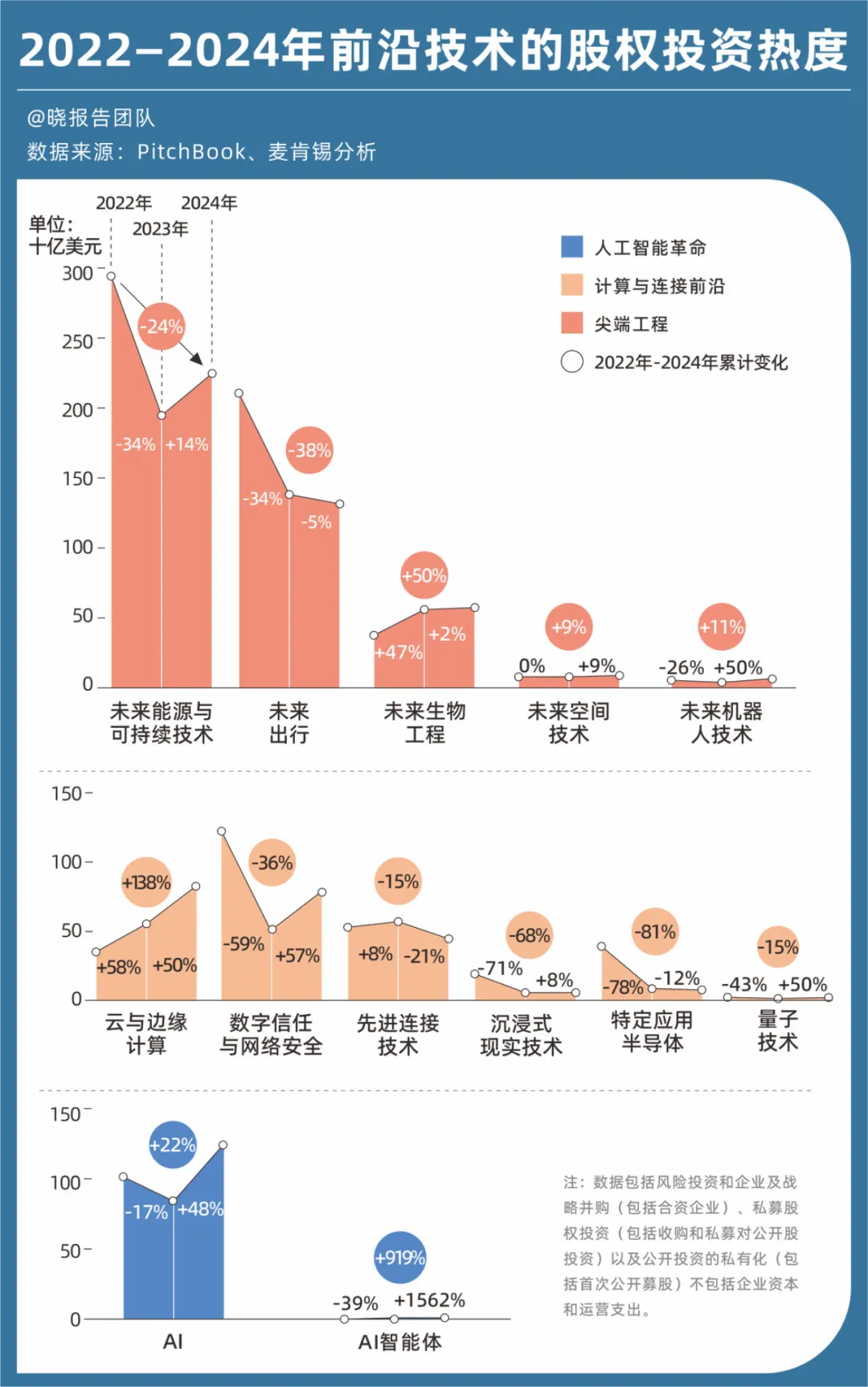

2024 年,這 13 項前沿技術的投資市場逐漸升溫,其中 AI、雲端與邊緣運算在投資規模及增速上表現尤為突出。

若以資本絕對聚集地而言,2024 年最「吸金」的五大前沿技術分別為:未來能源與永續技術(2232 億美元)、未來出行(1316 億美元)、AI(1243 億美元)、雲端與邊緣運算(808 億美元)、數位信任與網路安全(778 億美元)。

以成長勢頭來看,AI 智能體技術成長最快,2024 年投資額暴增 1562%;未來生物工程、雲端與邊緣運算則連續兩年融資額成長;AI 與未來機器人技術領域投資在短暫下滑後,2024 年已回升至高於兩年前的水準。

值得注意的是,與資本流向同步,人才爭奪戰也悄然展開。

麥肯錫報告指出,從徵才職缺數據來看,2024 年有 6 項前沿技術職缺需求成長,其中 AI 智能體職缺人才需求暴增 985%,AI、特定應用半導體職缺人才需求分別成長 35% 和 22%。以職缺類型來看,軟體工程師需求殷切。

這些人才技能需求比例反映一個殘酷現實:技術進化速度極快。相較之下,人才培育速度明顯不足。在 AI 與特定應用半導體兩大熱門技術領域,人才供需比例尤其失衡。

AI 對資料科學家的需求最為迫切,人才供需比例僅 0.5(即 2 個職缺搶 1 人才),企業爭相尋找能以 Python 處理資料及建模的人才。特定應用半導體領域更為極端——精通 GPU 架構與機器學習硬體的專家,供需比例低至 0.1,相當於十個職缺等一位合適人選。

未來機器人技術、未來生物工程等跨領域領域,則呼喚新型「跨領域人才」。未來機器人技術領域既需機械工程師,也需 AI、軟體工程人才,掌握人工智慧技能者人才需求比例為 0.2。未來生物工程領域,一位能設計機械手臂又能編程讓其智慧抓取的人才更為稀缺。

未來能源與永續技術、未來空間技術這兩個代表人類未來的領域,「人才荒」也更加明顯。例如掌握「綠色能源」,包括綠色能源、永續發展等專業知識的人才,供需比例低於 0.1。也就是說,每十個相關職缺,可能只有不到一位合格申請者。未來空間技術領域雖然整體職缺數量下滑,但對軟體工程師及 Python 專家的需求依然旺盛,每天都有大量衛星資料需要處理與分析。

這些數據顯示,未來人才培育僅具備程式能力已不足,「技術 + 場景」「軟體 + 硬體」「演算法 + 倫理」的複合型人才,將成未來十年最稀缺資源。

結語

回顧當下,站在科技大時代門口,中國正處於複雜且微妙的位置。

在應用層面,我們的成就令人矚目:5G 網路廣泛覆蓋、電動車高滲透率、光伏製造領先全球、無人機商業應用領先,這些皆屬中國產業優勢。但在基礎層面,半導體製造、底層 AI 模型、量子技術、生物醫藥原創技術等領域仍存在瓶頸風險。

美團無人機物流配送業務需求強勁

麥肯錫這份報告帶來的最大啟示也許是:未來競爭,不再是單一技術突破,而是生態系統、人才體系、價值觀的競爭。

聲明:

- 本文轉載自 [吳曉波頻道],著作權歸原作者 [ 巴九靈 ] 所有,如對轉載有異議,請聯絡 Gate Learn 團隊,團隊將依相關流程儘速處理。

- 免責聲明:本文所表達之觀點及意見僅代表作者個人立場,不構成任何投資建議。

- 文章其他語言版本由 Gate Learn 團隊翻譯,未經提及 Gate 情況下不得複製、傳播或抄襲已翻譯文章。

分享

相關文章

Jito 與 Marinade:Solana 流動性質押協議全面比較

JTO 代幣經濟學深入解析:分配結構、用途及長期價值

Cardano vs 以太坊:兩大主流智能合約平台的本質差異

Sentio vs The Graph:實時索引與子圖索引機制比較

ST 代幣有哪些用途?Sentio 生態激勵機制全面解析